Update 2/7/2023

The markets overall had a very strong January. The overarching theme for the month was a more favorable inflation outlook based on data that not only gave markets comfort that inflation has peaked and will trend lower in the coming months, but also led to speculation that inflation would decelerate sharply and the Fed would be cutting rates in the second half of the year. Expectation of interest rate cuts has led to visions of a soft landing for the economy amongst an increasing number of market participants and the view become increasingly priced across markets as the month progressed. 10-year yields began the year at 3.88 percent and fall to as low as 3.34% before reversing course in early February. Gold gained more than 7 percent through late January before reversing sharply lower, and the Nasdaq gained 10.72% for the month. That was the best January for the Nasdaq since January 2001. The swing in sentiment during the month was palpable and several sentiment indicators, though not all, are showing extreme readings that have coincided with market reversals. One example is the CNN Money Fear-Greed Index, which reached a reading of 79 (extreme greed) on February 2. That is its highest sentiment reading since the bear market began in early 2022 and suggests the recent rally, which we believe is another countertrend move similar to those seen that ended in late March and August last year, should be in its very late stages. The markets have likely gotten well ahead of themselves in pricing in Fed rate cuts later this year in light of the persistent strength in labor market indicators (payroll gains, job openings, unemployment, and low jobless claims) that are likely to sustain pressure on wages and service prices. Yields have jumped sharply, particularly for intermediate term maturities, since the employment indicators were released on Thursday and Friday of last week. CNN Fear and Greed Index

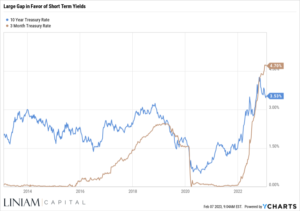

For the bond market, the decline in yields led to robust performance in January with the broad bond market up a little over 3 percent for the month. When the decline in longer term yields began approaching 3.5 percent in the latter part of the month we began to pare exposure across our managed portfolios. Further declines in long term yields seemed unlikely absent an about face in Fed policy in the relatively near term. Falling inflation readings alone will be insufficient to reverse Fed policy, the labor market will need to cool meaningfully from the pace of job creation in recent months and unemployment will need to move at least modestly higher from its current level. At the same time that longer term yields moved lower last month, short term yields continued to climb with 3-month Treasury yields rising to nearly 4.75 percent in anticipation of the Fed’s February rate hike. The yield advantage to short term bills, and the unlikely prospects for a further near-term decline in longer term bond yields, made for a compelling move from longer term bonds to short term bills. If longer term yields continue to reverse higher as they did on Friday, this move will be nicely additive to portfolio performance. We’ll look to move exposure back toward longer-term yields if or when they climb back above 3.75 percent or other information is indicative or material reductions in Fed policy rates.

As noted earlier, the Nasdaq index had its best January since 2001. Despite the strong January back then, the Nasdaq went on to decline by 50 percent in 2001 as the tech bubble continued to deflate. We see a similar set up for the markets this year at least in directional terms. Apple, Amazon and Google all reported earnings last Thursday after the close. Each stock fell by roughly 5 percent in afterhours trading on disappointing results. Despite weak results and the initial price reaction Apple closed up by better than 2 percent on Friday, which is pattern that was common during the corporate earnings reporting period where the market participants used price weakness following disappointing results to buy and ultimately drove share prices higher. The strongest segments of the equity markets in January where stocks that were last year’s weakest performers, stocks with the highest level of short interest, and tech companies that have no profitability. The overall performance of corporate earnings as being reported so for Q4 has not been strong. Equity performance in January has been driven by valuation gains on the hopes for further disinflation, interest rate reductions and recession avoidance as the year progresses. Equity markets are vulnerable to disappointments across any of these dimensions.

Global developments have also been a contributor to positive mood to begin the year, most notably the end of Covid lock downs in China and the unusually warm winter in Europe that allowed the Europeans to escape the constraints of a physical energy shortage associated with supply disruptions of natural gas. These are both positives relative to baseline expectations a couple of months ago, but the fundamentals are at odds with the downward movement in long term yields in January as both developments lift the global outlook relative to that baseline. The pressure for higher rates should persist in the near term, leading to pressure on those segments of the economy and companies most vulnerable to sustained higher borrowing costs. The escalation of hostilities in Ukraine and the increasingly adversarial relationship with China are growing sources of market uncertainty that in our view are inconsistent with the high valuations currently placed on equity markets.