Data Review and Market Update 11/30/2022

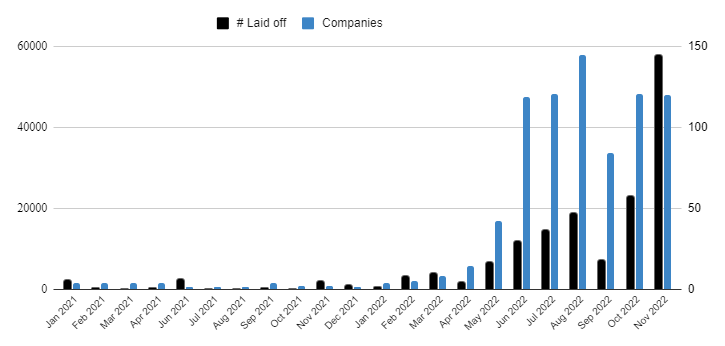

Today’s economic reports concerning the labor market continue to paint a mixed picture. The ADP employment report covering the private sector showed job gains of just 127,000 in November, the slowest pace since January 2021. In addition, layoffstracker.com shows a sharp rise in layoffs in November above the rising trend during the past 6 months. However, the Job Openings and Turnover data released by the Labor Department covering October showed overall job openings of 10.33 million, which remains well above the number of job seekers today and will keep the Fed’s concerns about wage pressure and inflation in place. We anticipate that job openings will decline in the coming months, and layoff data certainly points to a growing pool of available labor. But the gap between open jobs and job seekers remains too wide at this point to change the outlook for the Fed.

In other data, the Chicago Purchasing Manager Index for November released this morning points to a sharp contraction in manufacturing activity in region last month. The decline in the index to a reading of 37.2 is at level that last corresponded with the depths of the pandemic shutdown, the great financial crisis in 2008 and the 9/11 attacks. Pending home sales declined by 4.6 percent in October and were down by an astounding 37% on a year over year basis. The implication is that the rise in interest rates and dollar strength over the past 11 months have had a dramatic effect on economic activity in the most interest rate sensitive sectors of the economy, but to date have not sufficiently influenced labor market performance to alter the Fed’s policy trajectory.

In the past several cycles, data as weak as that seen in today’s manufacturing and housing data would have had the Fed easing policy to support the markets and by extension economic conditions. That is not the case today due to the underlying inflation picture and disequilibrium in the labor market. This implies that short term rates will remain elevated and perhaps the inversion of the yield curve will deepen further, suggests recession next year becomes even more likely, and should correspond to a further downward repricing in the equity markets as earnings are likely to be well below the consensus expectation of 5 percent growth next year.

Markets tend to view the above data points as second tier indicators to the monthly employment report which will be released this Friday. We anticipate that data will be consistent with the ADP report showing sharply slower job growth, but one month’s worth of data will not likely be sufficient to change the policy outlook.

Minneapolis, MN

(612) 760-2454

Please note the Liniam Capital LLC does not participate in any social media chat rooms. If for some reason we are represented as such, please be aware this is not our firm and should be considered false and fraudulent information.

Copyright © 2025 Liniam Capital All Rights Reserved